Your Business Is Profitable.

Your MCA Stack Is Eating It Alive.

We help B2B service providers refinance $100K–$10M in merchant cash advance debt into one structured facility — then optimize your credit profile and balance sheet so you never need an MCA again.

Stacked Advances Don't Just Cost Money.

They Wreck Your Whole File.

Daily Drafts Bleed Cash Flow

Factor rates of 1.3–1.5 pulled out daily or weekly can consume 15–30% of gross revenue — money that should fund payroll, growth, and margin.

Your Balance Sheet Looks Radioactive

Stacked short-term liabilities destroy your debt-service coverage and current ratio. Banks see the stack and decline before they see the business.

The Re-Up Cycle Never Ends

When the draft squeezes cash flow, the funder offers a "top-up." Each re-up digs the hole deeper — and adds inquiries that damage your credit.

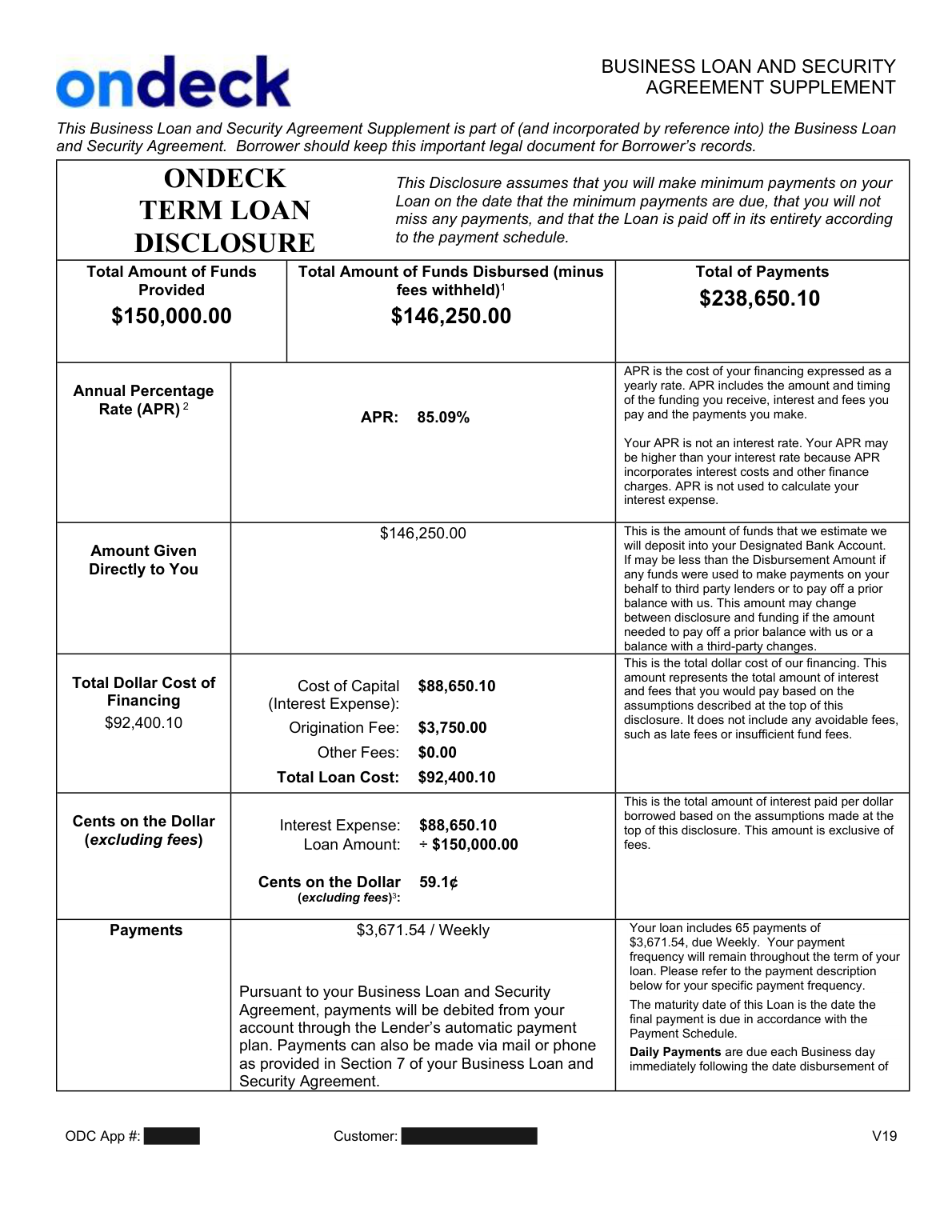

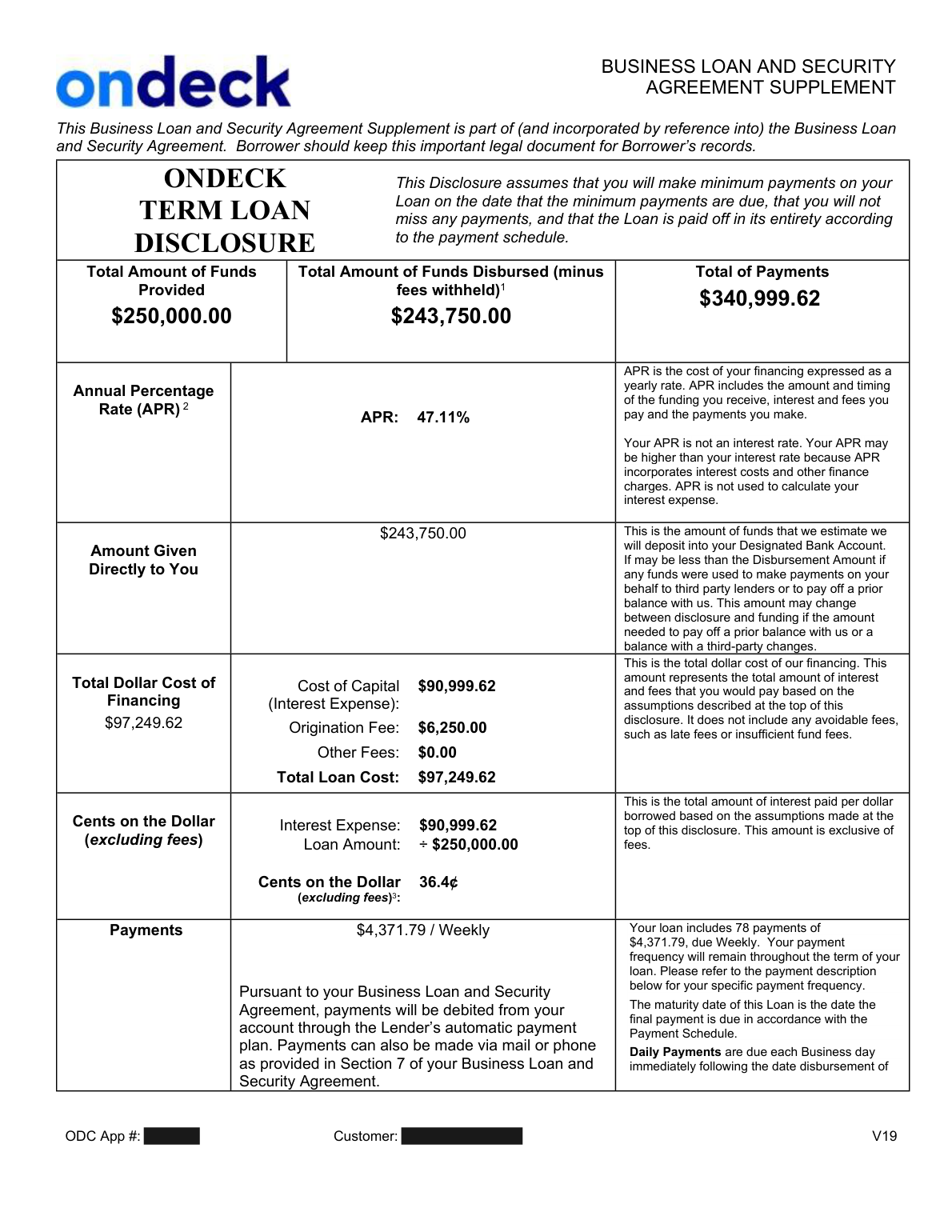

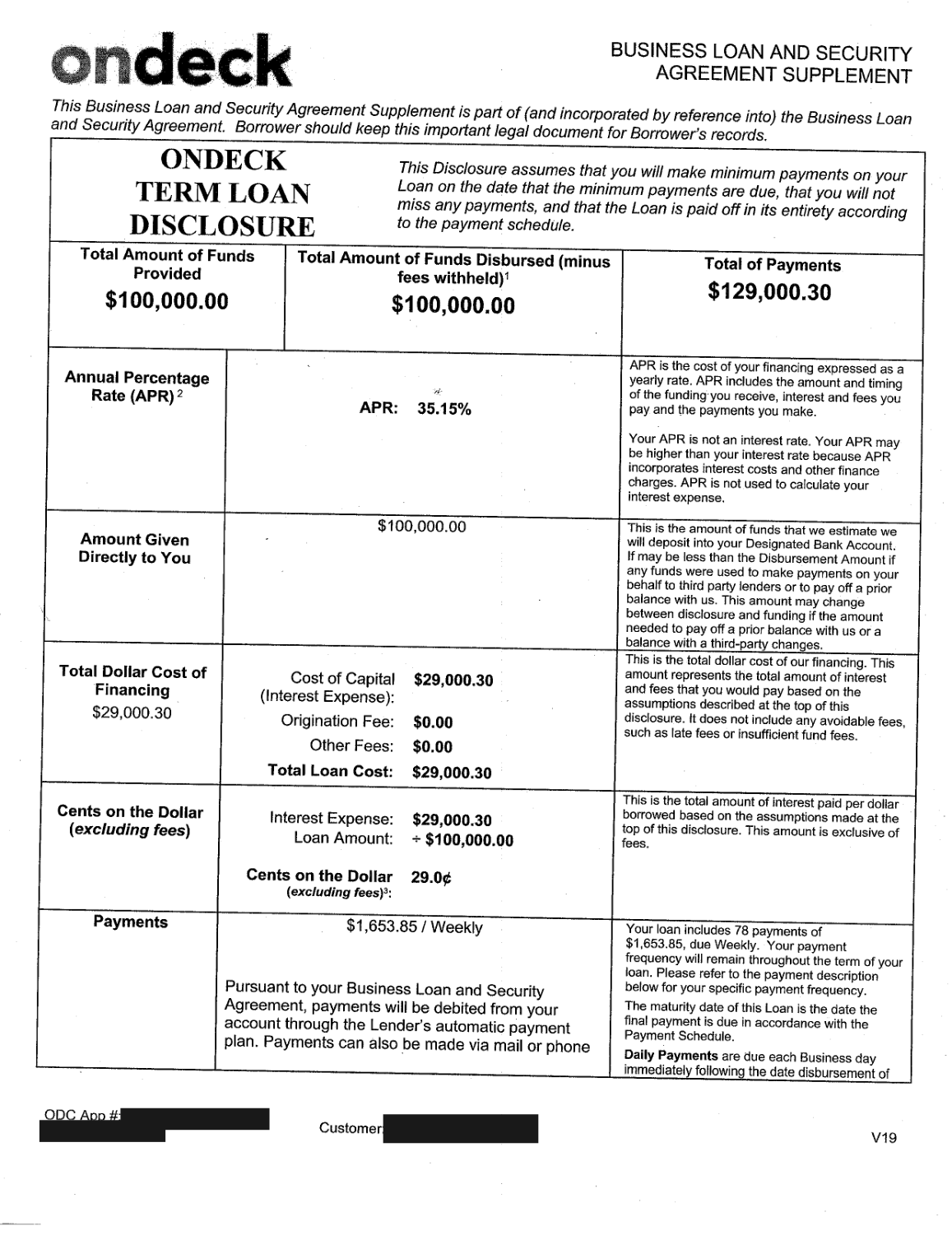

This Is What That Debt Actually Looks Like

These are three actual disclosures from client files — the kind of stacked short-term financing that quietly bleeds a business dry. Client details redacted for privacy. Look at the APRs, then look at the weekly payments.

leaving the account every month in weekly drafts across these three positions

paid in interest for every $1 borrowed on these files (59.1¢ / 36.4¢ / 29.0¢) — before fees

what the combined $500K could look like as one structured facility* — see the calculator below

Figures taken from three actual lender disclosures provided by clients; identifying information removed. *Refinance comparison is an illustration at 15% APR / 48 months — actual terms vary by credit profile and lender.

What Refinancing Your MCA Actually Saves

Drag the sliders to match your current position. We'll compare your MCA drain against a structured refinance and show the monthly cash flow you get back.

Your Numbers

*Illustration assumes refinancing the remaining payback into a 48-month facility at a 15% APR for comparison purposes. Actual rates, terms, and eligibility vary by credit profile, financials, and lender. This is not an offer of credit or financial advice.

Three Steps. One Bankable Business.

Refinancing alone treats the symptom. We fix the file that forced you into MCAs — then put it in front of the right capital.

Optimize the Credit Profile — Personal & Business

Every MCA application left hard inquiries on your file. Before anything goes to a lender, our AI dispute software cleans it up — targeting eligible inquiries not attached to an open account, with removals targeted in 72 hours.

- 72-hour hard inquiry removal (eligible Experian inquiries; TU & EQ add-on)

- Utilization, depth, and tradeline strategy

- Requires active MyFreeScoreNow or MyScoreIQ monitoring

Underwrite With Our 14-Point Scorecard — Know Before Lenders Do

Our underwriting team runs your file through the same 14-point credit scorecard our capital partners use — EBITDA, business and global DSCR, leverage, current ratio, borrowing base, and more — then optimizes the balance sheet so every metric tells a fundable story.

- 14-point scorecard across cash flow, coverage, and leverage

- Balance sheet restructuring — short-term MCA debt repositioned as long-term structure

- Lender-ready credit memo and financial package

Connect With Our Banks & Private Lenders — $100K to $10M

With a clean profile and a scored file, we place you directly with the banks and private lenders in our network who fund B2B service providers — consolidating the stack into one structured facility and killing the daily drafts.

- Matched to lenders whose credit box your scorecard already fits

- Term loans, revolving lines, and private credit facilities

- Payoff letters negotiated directly with your MCA funders

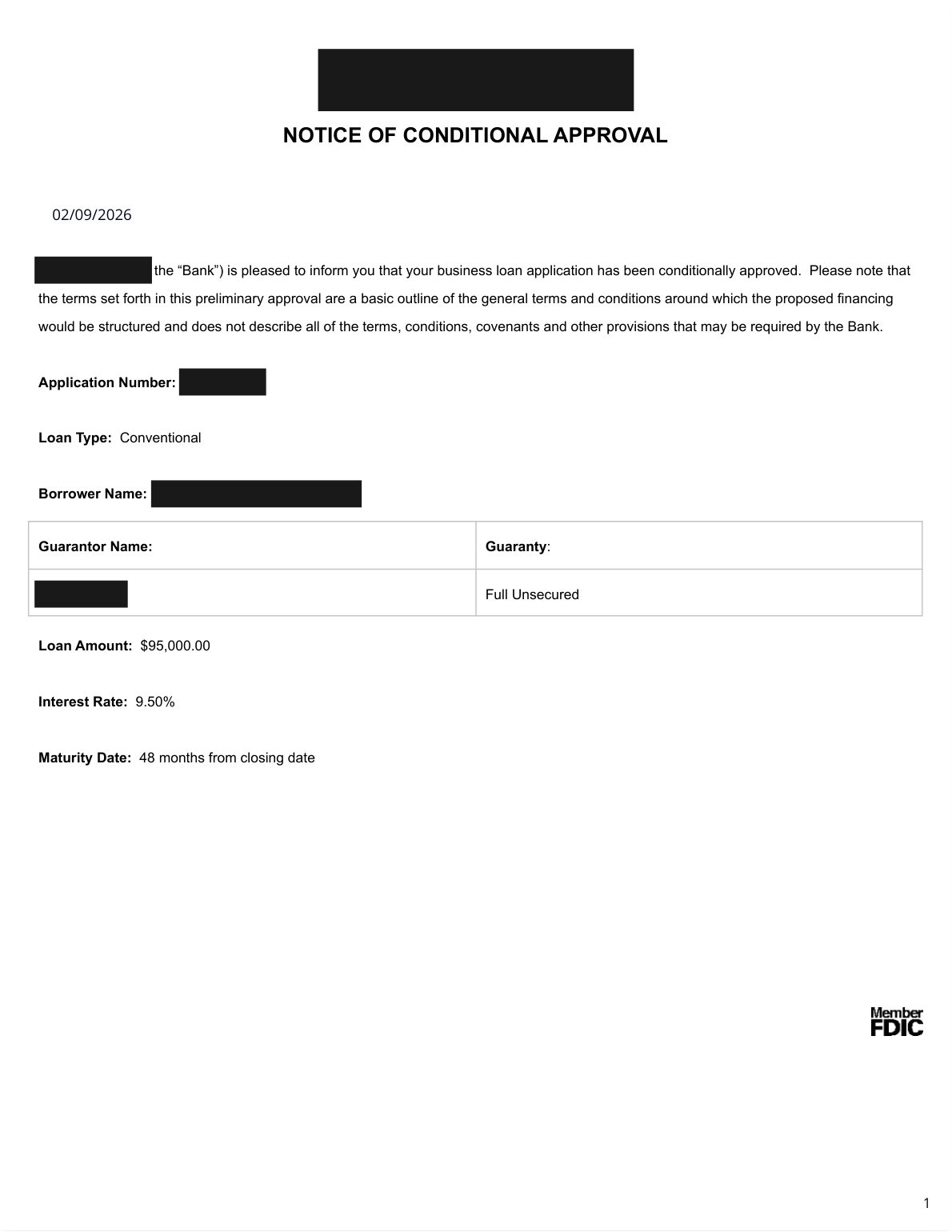

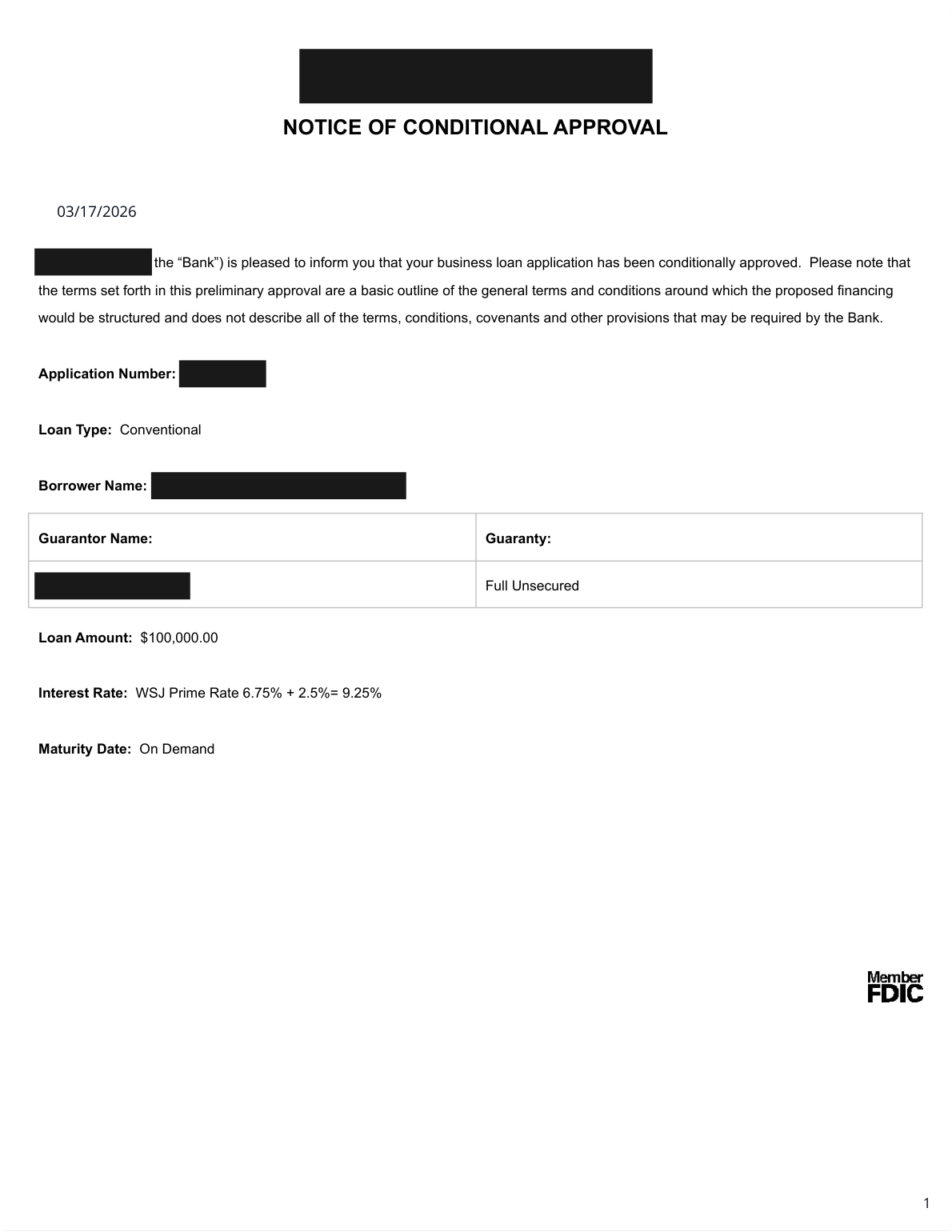

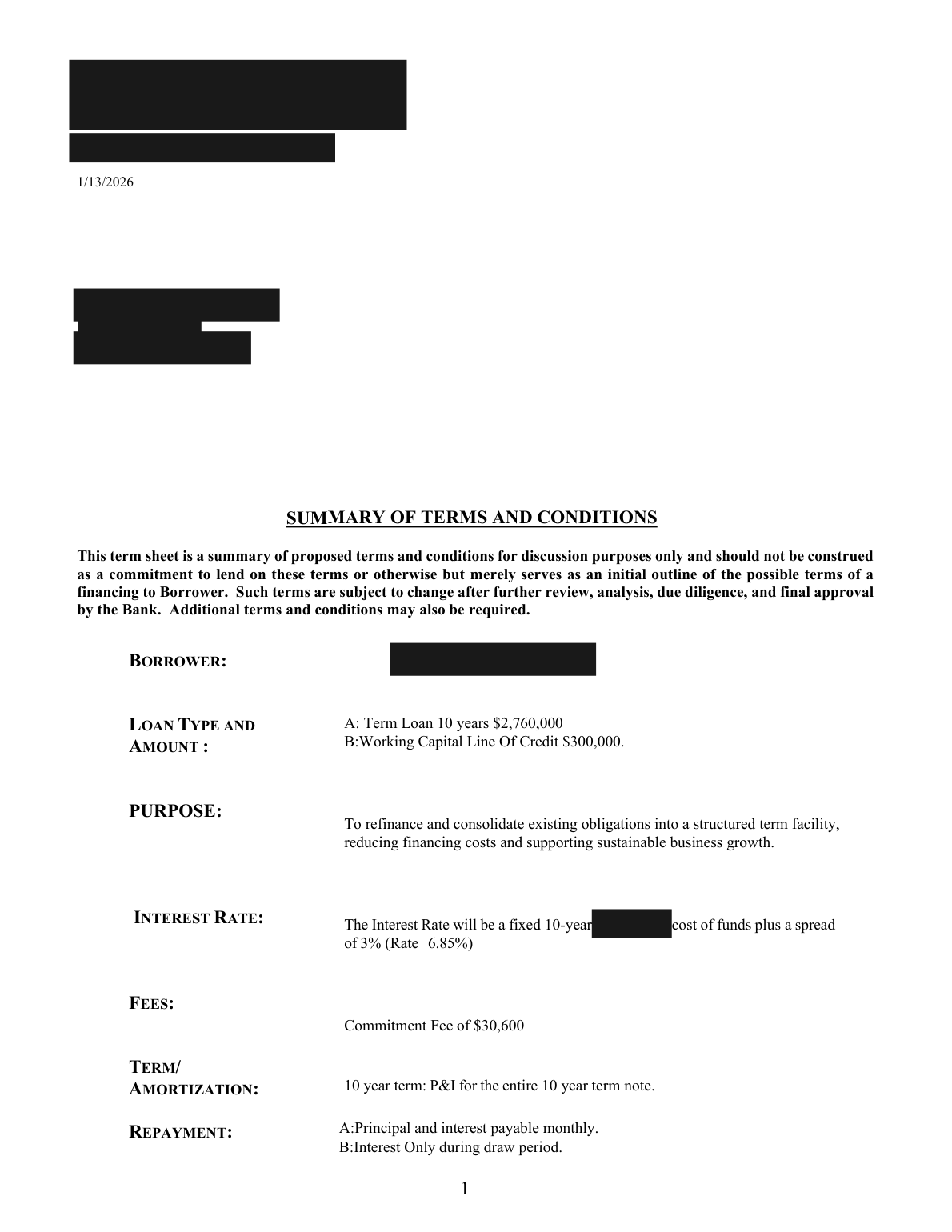

Real Bank Approvals. Real Letterhead.

Actual conditional approvals and a bank term sheet issued to our clients by FDIC-insured banks — single-digit rates, from unsecured working capital to a $3M+ MCA-consolidation refinance. Client information redacted; lender identities stay private until you're a signed advisory client.

Conditional approvals shown as issued by the lender; identifying information removed for client privacy. Approvals are conditional and subject to lender terms; individual results vary.

Two Paths Out. Here's What Each Requires.

Where your file goes depends on what you bring to the table. Most clients qualify for at least one path — and our credit optimization work exists to move you into the better one.

Bank Refinance

Single-digit rates on bank letterhead — like the approvals above. The gate is your credit profile.

- ✔700+ FICO score required — this is the threshold banks hold you to

- ✔Clean inquiry profile — our 72-hour removal gets you there

- ✔Financials that pass the 14-point scorecard

Below 700 today? That's exactly what Step 1 fixes.

Private Credit

Faster and more flexible when the score isn't there yet. The gate is collateral your business already owns.

- ✔Collateral required — outstanding accounts receivable

- ✔Inventory

- ✔Machinery & equipment

B2B receivables are an asset — we structure them into your borrowing base.

Built for B2B Service Providers

Manufacturers, agencies, staffing, IT services, commercial contractors, wholesale & distribution — businesses doing $750K–$10M in annual revenue with real receivables and real margins, stuck servicing debt built for someone else's balance sheet. If that's you, the fix is a 15-minute conversation away.

Keep the Business.

Lose the Daily Drafts.

Book a free 15-minute call. We'll review your positions, run your real refinance numbers, and map the credit and balance sheet fixes — no pressure, no obligation.

📅 Book My Free Refinance Review